1600 words (15 minutes reading time) by Colin Weatherby

Great post by Lancing Farrell. I like the link to the creative and enduring solutions people have devised in response to food scarcity. Human ingenuity can be a marvellous thing.

The impact of declining financial sustainability on asset management is disturbing. As anyone directly responsible for council assets knows, for many years the biggest challenge for local government in Victoria has been the cost of caring for assets. The Institute of Public Works Engineers (IPWEA) has been advocating for better asset management for years. I would argue that the principal council service is to own and care for assets on behalf of the ‘community. The rate cap has rapidly made this much more difficult, and as Lancing showed, the challenge is not spread evenly across councils.

What can councils do in response to funding scarcity? Will our commitment and creativity help us find new ways to provide the services the community needs and expects? Our own il comune povero.

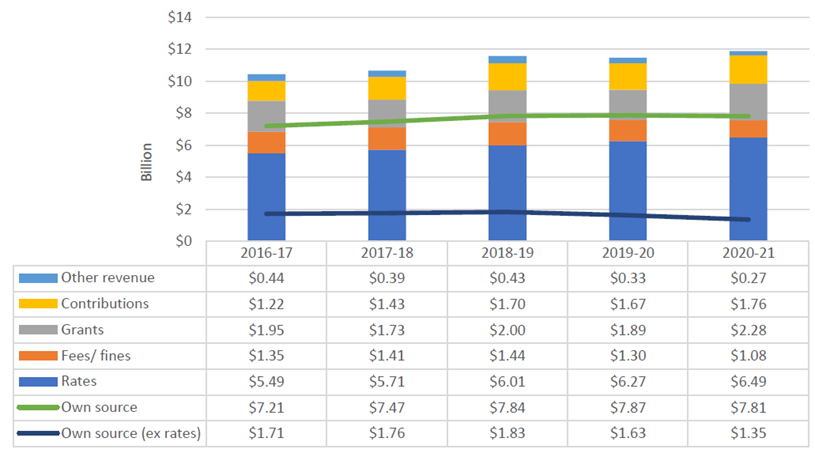

The obvious response is work out how to increase revenue. Council sources of revenue are shown in the graph above. Rates is the largest source of revenue, which explains why the rate cap has had such a rapid impact. In Victoria, rates can only be increased by the percentage allowed under the rate cap set by the Minister for Local Government. So far, councils have had very limited success in convincing the Minister to vary the cap from the amount recommended to them by the Essential Services Commission.

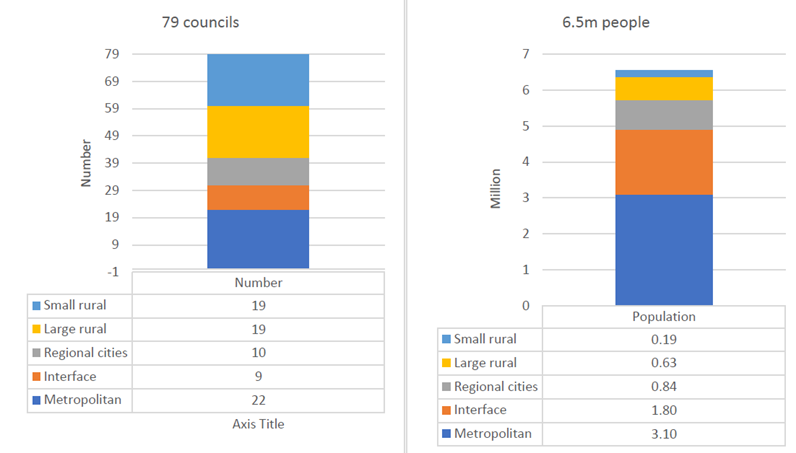

Individual councils have sought a rate cap exemption (i.e. this enables an increase to rates that is greater than the cap set by the Minister) with limited success. The criteria to be met are limited and the Minister must individually approve each application. An alternative to councils individually seeking a variation to the cap could be to change the method of calculating the cap. This could result in a cap across all councils that better reflects the actual cost increases councils are experiencing or a different rate cap for different types of councils. You can see in the graph below the differences in population (and ratepayers) across types of councils. Either approach would be fairer and require the Minister to agree.

Part of the challenge in removing or varying the rate cap is that it has the support of all major political parties in the Victorian parliament. Stopping another level of government from raising taxes is electorally popular. Applications can be made for an increase in the rate cap, however, they need to demonstrate community support for the increase. It is forcing communities to request higher taxation if they want local services. This is a big ask for any level of government, even when the value of its services is apparent to the tax paying public.

I’ll work my way through each of the potential revenue sources. Councils can currently increase fees or issue more fines. A barrier to this approach is that the Victorian government has indicated that it will start capping fee increases if councils increase them significantly as an alternative revenue measure. As the graph shows, fees and fines are a much smaller source of revenue anyway.

Fines, especially parking fines, have become an important source of revenue for some councils, especially in inner Melbourne. The reliance on fines by these councils became evident during the pandemic when parking demand reduced as people worked remotely and councils were directed to stop issuing some types of fines to reduce the burden on the community. In my experience, setting out to raise revenue by fining people isn’t reliable and usually gets push back from the community. It defeats the purpose of fines in achieving compliance and can’t raise enough revenue to solve the problem.

Grants are an important source of funds. Operating grants are usually tied to a particular service but there are some untied grants. Unfortunately, capital grants contribute to the asset ownership problem being created by the rate cap. They are usually to create new assets, which adds to the ongoing costs of operations.

‘Contributions’ are typically from developers and associated with urban development or redevelopment. They can create similar problems to capital grants. The contribution is either cash for the council to use to create new assets and new assets that are built by the developer and gifted to the council when subdivisions are completed. They add to the asset value and ongoing operating cost.

‘Other revenue’ includes interest and the proceeds of asset disposal, for example land sales. It is not a revenue source that can easily be increased. Some councils own commercial real estate and get rent, or they own a business that provides services commercially and returns a dividend, for example a landfill. It can be difficult to get into a money-making commercial venture – ratepayers tend not to like the council investing their money.

As you can see, raising revenue is not simple for councils under a rate cap. You can’t help thinking that is the whole idea. The alternative revenue sources are much smaller and difficult to increase. The added challenge is that the Minister has said they could also be capped if council try to use them to replace lost rates. Let’s have a look at expenses.

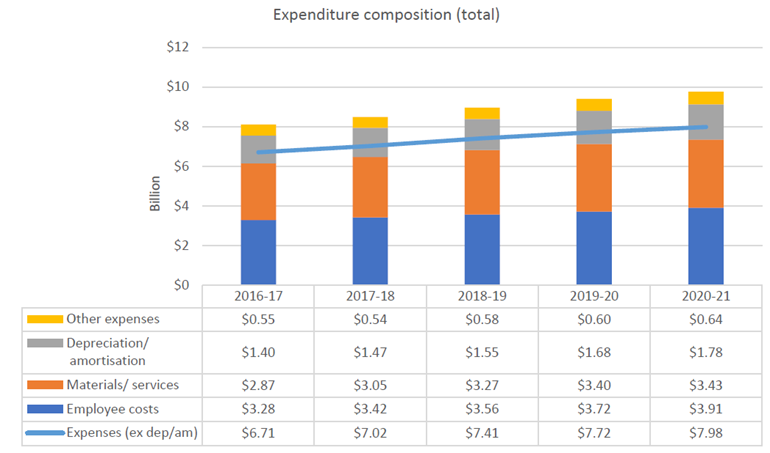

Anyone who has run their own business will know that when you can’t increase prices, after a while, costs will eventually exceed revenue. This is when you go out of business. Before that happens, you will have been trying to reduce expenses to stay in business. This is pretty much where Victorian councils find themselves.

As you can see in the graph above, the two main costs that councils have are employees and materials/services. Employee costs are all the usual labour related costs. Many of the services delivered by councils are labour intensive, whether that labour is provided by council employees or contractors working for the council. Materials and services expenditure also includes labour costs when contractors are engaged to provide services.

There are ongoing arguments in local government regarding the relative merits of councils delivering services themselves with their employees, or whether they should outsource service delivery to contractors. Proponents of outsourcing typically argue that it will reduce cost with the same or better service. How this is achieved seems to come down to lower wages and greater efficiency in operations. Sometimes this is because the ‘added extras’ provided by council workers are not provided.

Irrespective of whether a council delivers a service itself or outsources delivery, getting better at delivering the services is unlikely to solve the revenue problem. A colleague at one metropolitan council told me that the impact of the rate cap over 5 years, in comparison with the councils previous rating strategy and anticipated income, was now $40m less revenue. To be able to absorb that loss of income the council needs to reduce employee and materials/service expenditure by about 16%. Alternatively, less funds are available for capital works, which adds to the challenge of finding the capital required for asset renewal …

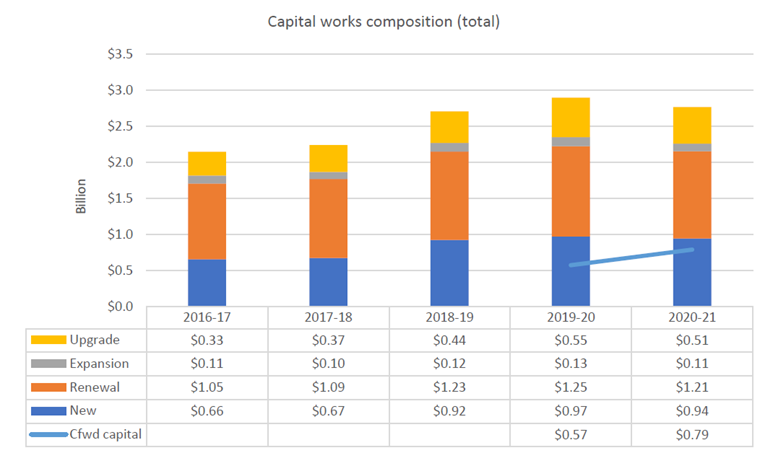

The funds available for capital works are what remains after operating expenses have been deducted from revenue, and councils have competing demands for that that capital. The first call on capital should be asset renewal. The graph above shows council spending on asset renewal as a percentage of depreciation. It illustrates the pressure on capital budgets. FinPro say that the failure to spend 100% of depreciation over a long period of time has resulted in a $1.9billion ‘asset renewal gap’. It is the cumulative amount that councils have not spent, and one day will need to spend to replace assets that have reached the end of their service life. The graph below shows how councils have spent their capital. It is worth considering whether councils are spending the capital that they do have in the best ways.

Most councils are putting a significant amount of their available capital into asset renewal but is has dropped from almost 50% of capital expenditure to 43% since the rate cap was imposed. The capital required for upgrade and expansion of assets has grown, and this expenditure is important to ensure assets remain ‘fit for purpose’. Having said that, when renewal is required it is seldom as simple as ‘like for like’ replacement because council assets have a long service life and new standards must be met. Funding for new assets is the second highest annual capital spend and reflects community demand for more services from their council.

Councils make continuous commitments of capital into multi-year delivery programs. This can quickly require more funds than are available, especially in an inflationary and rate capped environment. It is hard to keep track of demand. A useful exercise would be to calculate the funds required to provide 100% of depreciation for renewal of their assets in the next 3 years, then add the cost of completing all capital projects underway or planned to be completed in the next 3 years, and then adjust the estimated cost to include inflationary pressures. I think councils will be surprised by the cumulative demand.

My guess is that it is highly likely the capital demand will be way in excess of funds available. For most, if not all councils, the funds available for capital works when operating expenses are deducted from revenue have been declining as a percentage of revenue because operating expenses are growing faster than revenue. Demand for capital that exceeds available funds is the main pressure being put on council budgets by the rate cap and the response is often to reduce asset renewal funding.

The strategic challenge for councils is neatly described by John Lewis Gaddis when he talks about the alignment of ‘potentially unlimited aspirations with necessarily limited capabilities’. It is a fundamental ends and means problem – councils have to learn how to live within their financial means while still achieving the ends required by their community – il commune povero.

On Grand Strategy, 2018 by John Lewis Gaddis

State of Victorian Local Government Finances, October 2022 by Municipal Association of Victoria and Local Government Finance Professionals

Pingback: 239 – Zombie councils | Local Government Utopia