1000 words (10 minutes reading time) by Carole Davidson

The posts so far about the impact of the rate cap explain what is happening, but do they really help to work out what to do about it? Councils can tighten their belts and, perhaps, raise alternative revenues to replace lost rates. My question is will that be enough?

I thought I would go back to the beginning. Why did the Victorian Labor government think the rate cap was needed and what were they hoping to achieve? I am pretty sure that unless they see the changes in local government that they were after, they will not change their position. Even if they did, it is my understanding that the rate cap has bipartisan support, so the opposition will need to agree or they will simply reintroduce it if they win office.

The earliest information I can find is a report in The Age on 4 May 2014 saying that the then Labor opposition leader Daniel Andrews was promising a rate cap if his party were to be successful in the election being held in November that year. Their stated intention was to give ratepayers a ‘fair go’. Under the rate cap, councils would have to detail where every dollar they spend goes.

“The days of ratepayers footing the bill for Arnold Swarzeneggar impersonators are over”

Source: State councils must cap rates under Labor plan, The Age 4 May 2014

The reference to ‘Arnold Swarzeneggar impersonators’ suggests that Labor thought councils were wasting money. It refers specifically to a YouTube video made by the then Mayor and Deputy Mayor of Casey Council who were interviewed in a promotional piece about the Casey Cultural Centre project by an Arnold Swarzeneggar impersonator.

The clear message from Daniel Andrews was that Labor believed councils should keep rate increases in line with the Consumer Price Index (CPI) and that any rate increases above CPI would only be approved if the council could demonstrate a clear benefit to ratepayers.

“The promise was made by Opposition Leader Daniel Andrews in a staple electoral tactic that echoes similar electoral pledges by other state opposition parties in Australia as a way to exploit hostile voter sentiment to the cost of council services”.

Source: Vic councils slam Labor policy to cap rates at CPI, Government News, 6 May 2014

This is how the announcement was reported in Government News on 6 May 2014. Apparently, opposition parties across Australia at the time were promising to cap council rates because it was seen as an election winner. Government New reported a response from the Municipal Association of Victoria (MAV) President of the day. Bill McArthur. He said that rate capping was a failed Kennett (Liberal) government reform of the 1990s, which damaged development and liveability in all Victorian communities. Councils could only respond to a rate cap by reducing services relied upon by communities or reducing capital spending on assets.

In support of his second point, Bill McArthur highlighted the existing asset renewal gap of $225m, which was forecast to grow to $2.6b by 2026 unless there was serious intervention. Interestingly, the recent FinPro/MAV report cited by Lancing Farrell calculates the renewal gap in 2021 as being $1.9b. At this rate of increase, the renewal gap by 2026 will exceed $3b.

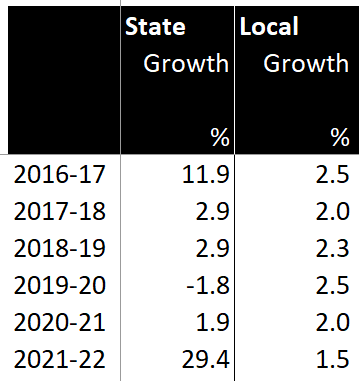

Bill McArthur also contrasted state taxes with local government rates and the increase over the previous decade. Council rates had increased from $1.8b to $4.3b ($2.5b increase) and state taxes from $9.3b to $15b ($5.7b increase). I suppose his point was, which is having the greater impact on cost of living for Victorians? He did ask whether a Victorian Labor government would limit state tax growth to CPI. Interestingly, State taxes since the Andrews government introduced the rate cap (2015/16 FY) have increased from $19.9b to $30.5b (2021/22). The table below shows the percentage increase in state taxes compared to the rate cap.

It would be interesting to calculate the average increases in actual revenues for both levels of government, with consideration of the compounding effects of the large increase by the state government in 2016/17. A similar increase for local government would have been helpful.

The Labor party, through the introduction of the rate cap. is clearly focused on making councils restrict their tax increases to the capacity of ratepayers to pay those increases (i.e. the same amount that the ratepayers can expect their income to increase – CPI). It assumes that council services are a basic commodity that should be able to continue to be delivered with only CPI increases. If any new or different services a community wants must be clearly identified and justified to the Minister for Local Government, who will then decide whether to approve a variation to the cap for a council.

Under this arrangement, any council wanting to offer more or better services to their community would need to convince the Minister of the merits through a public application process. It does seem to reduce the autonomy of councils to respond to changing community needs or preferences unless the state agrees.

Part 8A of the Local Government Act gives the state government the powers to introduce a rate cap and the purposes ascribed to a rate cap are interesting.

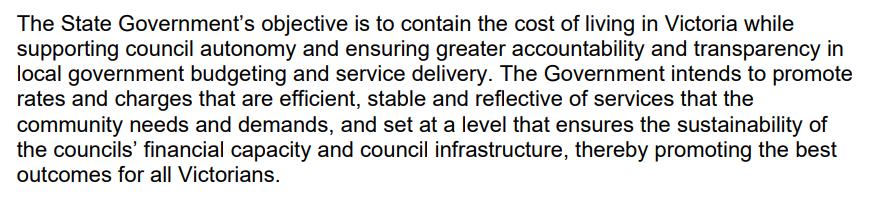

The Terms of Reference issued by the then Minister for Finance, Robin Scott, included a more detailed statement of the purpose of the rate cap.

The recent FinPro/MAV report on the financial sustainability of councils does raise the question as to whether the rate cap is ensuring the financial capacity of councils to perform their duties and exercise their powers. The most recent review of the rate cap by Grosvener Performance Group in 2021 only examined the mechanism for determining the cap. They did recommend a review to assess long term impacts with particular focus on the financial position of councils in 2026.

After five years of the rate cap it is apparent that councils are struggling to come to terms with its objectives. It has effectively suppressed council revenue but not demand for services and asset renewal. The impact on assets is cumulative and reduced expenditure now will create greater future liabilities. Based on what has happened in NSW, for every dollar a ratepayer saves today under the rate cap there will be debt and liabilities accruing on the council balance sheet that they must meet in the future.

Is 2026 going to be too late for a comprehensive review of the impact on the financial state of the sector?

State councils must cap rates under Labor plan, The Age, 4 May 2014

Vic councils slam Labor policy to cap rates at CPI, Government News, 6 May 2014

Final Report: Local Government Rate Capping Mechanism Review, Grosvener Public Sector Advisory, December 2021